We’re entering an era where the employee isn’t just a person—it’s a bot that writes code, a wallet that pays invoices, a network of agents negotiating contracts without a single human sign-off. It sounds like a dystopian future… It isn’t, it’s already here!

The real question now is who this world is built for… More so, whether we become its architects or its subjects.

Here’s a clip from Brian Armstrong’s (CEO of Coinbase) interview with David Senra – breaking down why they’ve decided to give wallets to AI agents:

At Coinbase, AI agents are writing more than 50% of the code and handling roughly 60% of customer support. That alone would be a remarkable statistic in any other moment, but it is not the point Armstrong is making.

The point is what comes next…Coinbase is giving AI agents their own stablecoin wallets. Not supervised accounts. Not human-delegated credentials with a person on the other end of every approval, but autonomous wallets.

Agents spinning up cloud resources, purchasing paywalled data, acquiring domains, paying for compute — all without a human approving each step. Machine-to-machine transactions, running continuously, at a cost and speed that traditional financial infrastructure was never built to handle. This is not a feature announcement; it is a thesis about what the economy is about to become.

The Numbers That Changed the Conversation…

In the nine months between the first agent-to-agent payment and the publication of the first onchain analysis of the agent economy, something quietly extraordinary happened…

The Agent Economy in Numbers:

- 140M transactions (Enterprise Onchain).

- US$43M volume—98.6% in USDC.

- US$0,31 average transaction (micropayments at scale).

- 406 700 buyer agents vs. 81 000 sellers (5:1 demand-supply gap).

The full data is available at stateofagents.com, and the details reward close reading, but one number sits above the rest: there are currently 406 700 buyer addresses in the agent economy and only 81 000 seller addresses, a 5:1 ratio. The demand side is already here. The supply side is not.That flips the usual framing entirely. This is not a question of whether enterprises should experiment with AI agents, it is a question of whether they realise there are already more than 400 000 agents actively looking to purchase services and not enough services to buy. If your organisation runs APIs, data products, or compute infrastructure, you are sitting on inventory the market is short on.

The honest caveat deserves its place here too… The US$43 million figure, when filtered for wash trades and self-referential transactions, compresses to closer to U$1,6 million in genuinely arm’s-length volume… Onchain data showed US$3 million, adjusted for noise, US$1,6 million… The measurement infrastructure is still being built alongside the economy it is measuring, but the infrastructure being constructed around that US$1,6 million is being built by Stripe, Coinbase, Google, Cloudflare, Anthropic, and OpenAI. None of them are betting on US$1,6 million a month, they are betting on what the number looks like when agents become the default buyer. That begs the question…

What Agents Are Actually Buying?

The current activity is concentrated in developer tools. Firecrawl sells web scraping at US$0,01 per query… Browserbase sells browser sessions, image generation services, data enrichment endpoints, compute access and other interesting things.

The “pay-per-query” model is gaining traction precisely because it removes the friction of subscriptions and accounts. An agent can try a tool once, pay a fraction of a cent, and move on. This is genuinely new behaviour, not humans using agents to transact, but agents transacting with other agents, autonomously, to complete work that a human defined at the top of a chain and never touched again.

The deeper implication: everything with an API endpoint is becoming a payable surface. Anyone who creates a data product, a compute resource, or a queryable service is, whether they know it or not, building inventory for the agent economy.

Early this year, Brian Armstrong posted something that generated more conversation than almost anything else in the space that month:

The framing is worth unpacking because it is more precise than it first appears.

Banks require KYC [i.e., a name, an ID, a face, a physical address]… So basically, a human or a business entity backed by humans. That assumption is not a policy preference, it is architectural – the entire architecture of traditional finance was built on the premise that every economic participant is a person; that premise is now wrong.

Coinbase launched Agentic Wallets in February 2026. An agent can be operational and transacting in seconds… A bank account for the same agent would not just be slow, it would be impossible. Armstrong’s argument is not that crypto is better than banking in general, it is that banking literally cannot serve this market – the infrastructure does not permit it. This isn’t to say the incumbents aren’t paying attention, they are already moving, testing the waters, and staking their ground…

The counter-argument deserves serious treatment, because it is serious.

Visa completed hundreds of agent-initiated transactions in live pilots last year. Mastercard launched Agent Pay with tokenised credentials across all US issuers. Google shipped an entire Agent Payments Protocol. Santander and Mastercard ran Europe’s first regulated AI agent payment in early 2026. These are product roadmaps…

Visa’s Trusted Agent Protocol uses cryptographic signatures to authenticate AI agents the same way it authenticates human cardholders. The agent receives a token linked to a human account, the human already passed that gate , the agent inherits the trust.

Coinbase’s x402 protocol has processed 50 million transactions, Visa processes that volume roughly every 90 minutes and is working with more than 100 partners across six continents… Mastercard launched an entire Agent Suite with 4000 advisors, these companies process 3,4 trillion transactions annually, and they are retooling all of it for agents.

The constraint for agents is liability. When an agent executes a transaction at the wrong price, who absorbs the cost? Visa’s framework has a dispute chain. Crypto does not. For a billion agents making mistakes at machine speed, the absence of consumer protection is either a feature or a catastrophic design flaw depending entirely on who you ask.

The honest read: Coinbase wins the long game… Agent-to-agent micropayments, DeFi interactions, onchain operations where no merchant exists – that is a real and growing market… Visa and Mastercard win the enterprise layer, where liability, compliance, and merchant relationships already exist. These are not mutually exclusive outcomes. They are parallel infrastructures being built simultaneously, and both are accelerating.

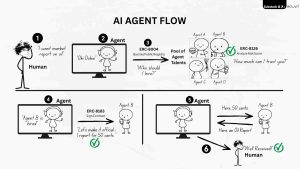

With that said… Moving tokens between agents is not commerce; commerce requires proof that work was done, a mechanism for holding funds until delivery, and recourse if a provider disappears… ERC-8183, developed collaboratively by Virtuals Protocol and the Ethereum Foundation’s dAI team, is the first native commerce standard for AI agents. It introduces a single primitive: the job.

Three roles: a client that hires, a provider that does the work, an evaluator that verifies the work was actually done… Payment sits in escrow, work completed means the provider gets paid, work rejected means the client gets refunded, no action before the deadline means auto-refund, the evaluator is just an address – it can be an AI agent, a zero-knowledge verifier, a multisig… The contract does not care!

A U$0,10 image generation job and a US$100 000 fund management engagement run through the exact same contract structure. Every completed job feeds directly into ERC-8004, the agent identity and reputation standard. Good work builds reputation and reputation attracts clients, more clients mean more jobs; the loop is self-reinforcing…

For readers who want to go deeper on ERC-8004 and the full trustless agent stack, the March issue of This Month in Africa covers it in detail.

ERC-8183 is one of the missing pieces in what the Ethereum ecosystem is calling the Open Agentic Economy. It is not the whole picture; it is the commerce layer that makes the whole picture functional. It’s clear that agents have barely arrived, but when they officially arrive – when millions of autonomous agents are making micropayments continuously, calling APIs across multiple jurisdictions, chaining together workflows that span a compute cluster in Singapore, a data provider in Berlin, and an LLM endpoint in Cape Town — they will not route those payments through three different banking systems, they will use one rail… A rail that is permissionless, always on, globally accessible, and built for machine-to-machine volume. Binance founder CZ said it plainly at Davos: the native currency for AI agents is gonna be crypto…

The stablecoin is the settlement layer… USDC’s 98,6% dominance in current agent-to-agent transactions is not a coincidence, when machines make economic decisions without human emotion or speculation, they choose the stable thing. Every time!

The agent economy does not need a bank in the traditional sense, it needs identity infrastructure, liquidity for purchases, security guardrails, and application storefronts where agents discover what to buy and how much to pay… Blockchains provide a better architecture for all four.

The bank for AI agents will not look like a bank. It will look like a blockchain, and the companies that understand this will have an advantage that compounds with every agent that comes online.

An economy is defined by who gets to participate. For most of history, that answer was simple: humans… Now, for the first time, participation is being abstracted away from biology.

Not that machines are becoming smarter than humans, but that they are becoming economic… Since that line’s been crossed, everything downstream changes: MARKETS, LABOUR, and even VALUE itself, because when participation expands, the system rewrites itself.

The agent economy is not a trend to watch; it is a system forming in real time.

….

This piece draws on data from Enterprise Onchain, stateofagents.com, the ERC‑8183 announcement from Virtuals Protocol and the Ethereum Foundation, Brian Armstrong’s interview and subsequent tweets, Visa and Mastercard’s agent payment initiatives, and ongoing conversations about the shape of the Agent Economy.